How to Build an Audit-Proof Business

Most business owners assume audits happen because someone did something wrong.

In reality, many audits begin because of missing documentation, poor bookkeeping, inconsistent reporting, or financial records that raise questions.

The good news is that building an audit-proof business is not about avoiding the IRS.

It's about creating systems that allow your business to confidently support its financial decisions.

For businesses generating $1 million or more in revenue, strong financial systems are no longer optional. They are essential for protecting profitability, reducing risk, and supporting long-term growth.

Direct Answer

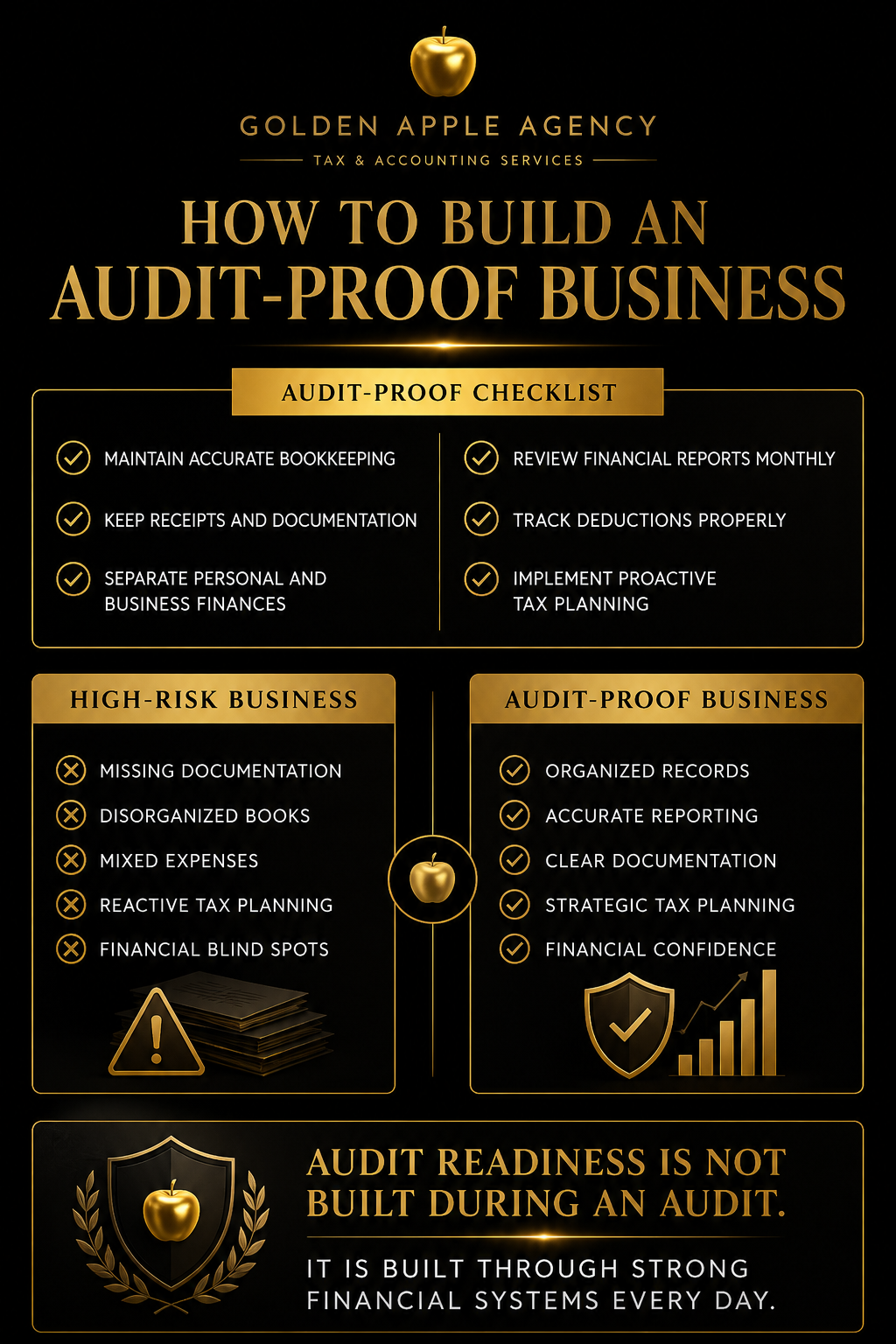

An audit-proof business is built through accurate bookkeeping, organized documentation, proactive tax planning, and strong financial systems. While no business is completely immune to an audit, businesses with clear records and financial controls are significantly better prepared to defend their positions if questions arise.

1. Maintain Accurate Financial Records

Your financial records tell the story of your business.

If that story is incomplete, inconsistent, or disorganized, it creates unnecessary risk.

Every audit-ready business should maintain:

Accurate bookkeeping

Monthly reconciliations

Organized financial reports

Proper expense categorization

Clear revenue tracking

Financial visibility is the foundation of audit readiness.

Without it, everything else becomes more difficult.

2. Document Every Business Expense

One of the most common reasons deductions are challenged is a lack of documentation.

Many business owners can remember why they spent money.

The IRS wants proof.

For significant expenses, maintain:

Receipts

Invoices

Contracts

Proof of payment

Documentation of business purpose

The deduction is only as strong as the documentation supporting it.

Good records eliminate unnecessary questions.

3. Separate Personal and Business Finances

Mixing personal and business expenses creates confusion.

It also creates audit risk.

Businesses should maintain:

Separate bank accounts

Separate credit cards

Clear accounting procedures

Consistent reimbursement policies

The cleaner the separation, the easier it becomes to support financial transactions.

Professional businesses operate with professional financial boundaries.

4. Review Financial Reports Monthly

Many business owners only review their numbers during tax season.

That approach often allows mistakes to go unnoticed for months.

Audit-ready businesses review:

Profit and Loss Statements

To monitor profitability and identify unusual transactions.

Balance Sheets

To verify assets, liabilities, and account balances.

Cash Flow Reports

To understand how money moves through the business.

Regular reviews help identify issues before they become larger problems.

5. Build a Proactive Tax Strategy

Tax preparation and tax strategy are not the same thing.

Businesses that only think about taxes once a year are often reacting.

Businesses that review taxes quarterly are planning.

Proactive tax planning helps:

Strengthen documentation

Support deductions

Improve compliance

Reduce surprises

Create strategic opportunities

The strongest businesses treat tax strategy as part of their growth plan.

Audit-Proof Business vs High-Risk Business

High-Risk Business

❌ Missing documentation

❌ Disorganized bookkeeping

❌ Mixed personal and business expenses

❌ Reactive tax planning

❌ Limited financial visibility

❌ No internal financial controls

Audit-Proof Business

✔ Organized records

✔ Accurate bookkeeping

✔ Clear financial separation

✔ Monthly reporting reviews

✔ Proactive tax strategy

✔ Strong financial systems

Reality Check

Many businesses focus heavily on growth while neglecting the financial systems supporting that growth.

Revenue growth without financial controls often creates additional risk.

The businesses best positioned for long-term success are not necessarily the ones generating the most revenue.

They are the ones that understand their numbers, document their decisions, and maintain strong financial processes.

Audit readiness is not created when an audit notice arrives.

It is created through the daily habits and systems of the business.

Final Thoughts

An audit-proof business is not built overnight.

It is built through intentional financial management, consistent documentation, and proactive planning.

As your business grows, the complexity of your finances grows with it.

The stronger your systems become, the more confidently you can navigate growth, profitability, and compliance.

The goal is not simply to avoid problems.

The goal is to build a business that can confidently support every financial decision it makes.

If your business had to explain every deduction, transaction, and financial decision today, would your records support it?

Strong businesses don't prepare for audits after they happen.

They build audit readiness into their financial strategy every day.